Debt Consolidation Loan Online: A Complete Guide

Managing multiple debts can feel overwhelming. If you’re juggling credit cards, medical bills, or personal loans, you may struggle to keep track of payments. Interest rates pile up, and your credit score can suffer. For many people, a debt consolidation loan online offers a practical solution. This guide will help you understand how online debt consolidation works, who it’s best for, and how to apply — all in clear, simple language.

What Is An Online Debt Consolidation Loan?

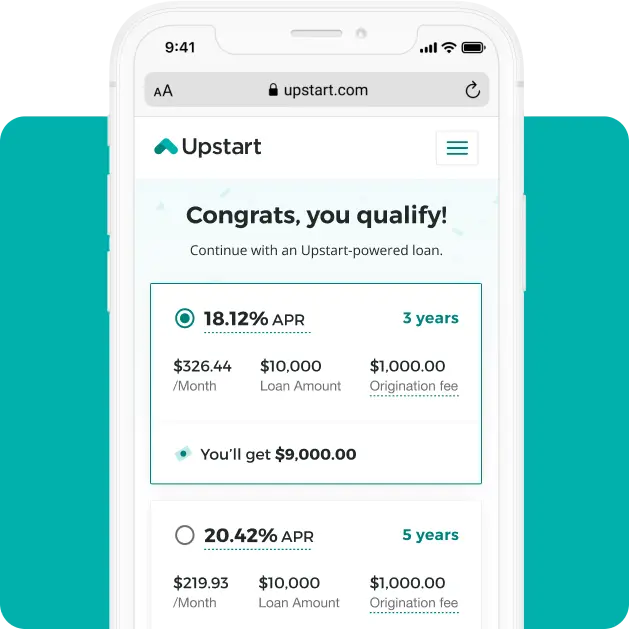

A debt consolidation loan is a new loan you use to pay off existing debts. Instead of making several payments each month, you only make one payment to the new lender. Online debt consolidation loans are offered by banks, credit unions, and online lenders. You apply through a website or app, and the process is usually faster than visiting a branch.

Imagine you have three credit cards with different interest rates. You take a debt consolidation loan online, pay off those cards, and now have one monthly payment at a lower interest rate. This approach can save you money, reduce stress, and help you become debt-free faster.

How Debt Consolidation Loans Work

The process is straightforward:

- Apply online: Fill out an application on the lender’s website.

- Approval and terms: If approved, you get a loan offer with details like interest rate, monthly payment, and repayment period.

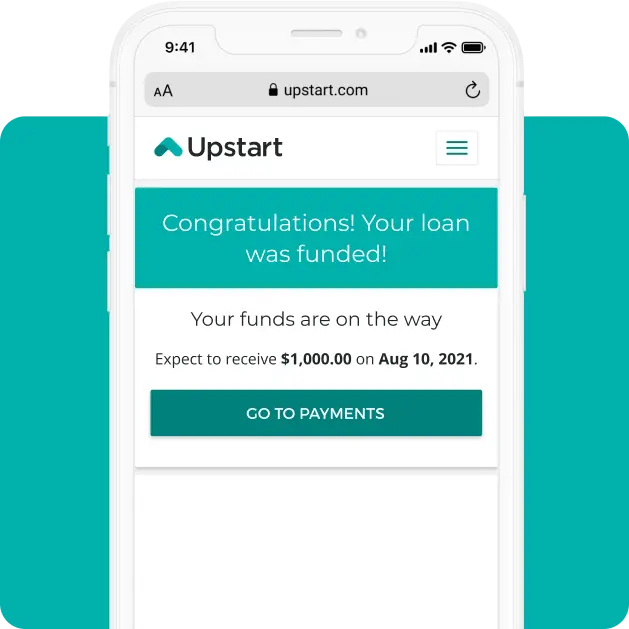

- Pay off debts: Use the loan funds to pay your old debts.

- Make one payment: Pay the new lender each month, often at a lower rate.

Many online lenders offer quick decisions. Some approve loans in minutes, while others take a day or two. Funds are sent directly to your bank account or used to pay creditors.

Benefits Of Debt Consolidation Loan Online

Debt consolidation loans offer several advantages, especially when managed online:

- Lower interest rates: If your credit is good, you might qualify for a rate lower than your credit cards.

- Single monthly payment: Easier to manage than multiple bills.

- Improved credit score: Paying off high-interest debts can boost your score over time.

- Fixed repayment schedule: You know exactly when your debt will be paid off.

- Fast process: Online applications are often quicker and simpler.

Here’s a comparison of typical interest rates for different types of debts:

| Debt Type | Average Interest Rate (%) |

|---|---|

| Credit Cards | 17–25 |

| Personal Loans (online) | 6–15 |

| Medical Debt | 0–8 |

Who Should Consider Debt Consolidation Loans?

A debt consolidation loan online is not the right choice for everyone. It works best for people who:

- Have multiple debts with high interest rates.

- Can qualify for a new loan with a lower interest rate.

- Want to simplify their payments.

- Are committed to paying off debt, not adding new charges.

If your credit score is low, you may not qualify for a good rate. In this case, consider other options like credit counseling or debt management programs.

:max_bytes(150000):strip_icc()/debtconsolidation.asp-final-18e80676e0af4379a7962bfc4a0874de.png)

How To Apply For A Debt Consolidation Loan Online

Applying online is simple, but you need to prepare:

- Check your credit score: Lenders use your score to decide your rate.

- List your debts: Write down each debt, balance, and interest rate.

- Compare lenders: Look at rates, fees, and reviews.

- Fill out application: Provide your income, employment, and debts.

- Receive loan offer: Review terms carefully before accepting.

- Pay off debts: Use funds to clear your old balances.

Here’s a comparison of popular online lenders:

| Lender | Minimum Credit Score | Loan Amount ($) | APR Range (%) | Time to Funding |

|---|---|---|---|---|

| SoFi | 680 | 5,000–100,000 | 6.99–22.28 | 2–7 days |

| Marcus by Goldman Sachs | 660 | 3,500–40,000 | 6.99–24.99 | 1–3 days |

| Upgrade | 580 | 1,000–50,000 | 8.49–35.99 | 1–4 days |

Key Factors To Compare When Choosing A Debt Consolidation Loan

Not all loans are equal. Here’s what matters most:

- Interest rate (APR): Lower is better. Compare total cost, not just monthly payment.

- Fees: Watch for origination fees, late fees, or early payoff penalties.

- Loan term: Shorter terms mean higher payments but less interest.

- Reputation: Choose lenders with good reviews and clear policies.

- Customer support: Reliable help matters, especially if you need guidance.

Many beginners miss one key detail: the impact of fees. Some loans have low rates but high upfront charges, making them less attractive. Always ask about all fees before accepting a loan.

Common Mistakes To Avoid

Debt consolidation can help, but only if used wisely. Here are common mistakes:

- Ignoring fees: Origination fees can add hundreds of dollars.

- Not checking credit score: Applying without knowing your score may hurt your credit.

- Choosing a long loan term: Lower payments sound good, but you pay more in interest.

- Failing to change habits: If you keep using credit cards, you may end up deeper in debt.

- Missing payments: Late payments can hurt your score and add fees.

A non-obvious insight: Many people forget to close old credit card accounts after paying them off. Keeping them open can help your credit utilization ratio, but if you’re tempted to spend, consider closing them.

Real-life Example: How Debt Consolidation Helps

Let’s look at a practical case:

Maria has $10,000 in credit card debt at an average interest rate of 20%. Her minimum payments are $250 per month. She applies for a debt consolidation loan online and gets approved for a $10,000 loan at 8% interest for 36 months.

Her new payment is $313 per month. She will be debt-free in three years, instead of paying minimums for many years and spending much more on interest.

Here’s a side-by-side comparison:

| Debt Type | Interest Rate | Monthly Payment | Total Interest Paid | Time to Pay Off |

|---|---|---|---|---|

| Credit Cards | 20% | $250 | $4,000+ | 5+ years |

| Consolidation Loan | 8% | $313 | $1,260 | 3 years |

Tips For Success With Online Debt Consolidation

If you want to get the most from your debt consolidation loan online, follow these tips:

- Make payments on time: Set up automatic payments if possible.

- Don’t take new debt: Avoid new credit cards or loans while repaying.

- Review your budget: Make sure you can afford the new payment.

- Check for discounts: Some lenders offer lower rates for autopay or good credit.

- Ask questions: If you don’t understand a term, ask the lender.

Another insight: Many online lenders allow you to check your rate without affecting your credit score. Use this feature to shop around before applying.

Alternatives To Debt Consolidation Loan Online

If you don’t qualify, or a loan isn’t right for you, consider these options:

- Balance transfer credit card: Offers low or 0% interest for a limited time.

- Debt management plan: Work with a credit counselor to create a plan.

- Snowball or avalanche method: Pay off debts one by one, starting with smallest or highest interest.

- Negotiate with creditors: Some will lower rates if you ask.

Each option has pros and cons. For example, balance transfer cards require good credit, and debt management plans may affect your credit score. Research carefully to find the best fit.

How Online Lenders Protect Your Data

Online lenders use strong security to protect your personal data. Look for:

- Encryption: Websites should use HTTPS.

- Privacy policy: Read how your information is used.

- Verified reviews: Check independent sites for feedback.

Always use lenders with clear contact information and good reputation. If an offer sounds too good to be true, it probably is.

Frequently Asked Questions

What Credit Score Do I Need For A Debt Consolidation Loan Online?

Most lenders require a credit score of 580 or higher, but better scores get lower rates. Some lenders accept scores as low as 500, but rates are much higher. Check your score before applying.

Does Debt Consolidation Hurt My Credit?

Applying for a loan causes a hard inquiry on your credit report, which may lower your score slightly. However, paying off debts and making on-time payments can improve your score over time.

How Long Does It Take To Get Funds From An Online Lender?

Many online lenders send funds within 1–7 days after approval. Some offer same-day funding, but most take a few days to process your application and verify your information.

Can I Consolidate Student Loans With A Debt Consolidation Loan?

You can use a personal loan to pay off private student loans, but federal student loans have special rules and protections. Always check before consolidating student loans — you may lose benefits.

Are There Risks With Debt Consolidation Loans Online?

Yes. Risks include paying higher fees or interest, missing payments, and getting deeper in debt if you don’t change spending habits. Always read the terms and make a plan before applying.

If you want more information on debt consolidation loans, visit the Consumer Financial Protection Bureau for official advice.

Debt consolidation loans online can help you take control of your finances, reduce stress, and save money. But success depends on choosing the right loan, understanding the terms, and committing to a clear repayment plan. Take your time, compare options, and ask questions.

With careful planning, you can move closer to a debt-free future.

Read More:

- Best Personal Loan Rates: Unlock Top Offers for 2026

- Bad Credit Personal Loans Guaranteed Approval: Easy Access Today

- Compare Mortgage Lenders Online: Find the Best Rates Fast

- First Time Home Buyer Loan Programs: Your Ultimate Guide 2026

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Small Business Loan Pre Approval: Fast Track Your Funding Success

- Mortgage Pre Approval Online: Fast-Track Your Home Buying Success

- Best Mortgage Refinance Rates: Unlock Lower Payments Today