Home equity loans are a popular way for homeowners to borrow money using the value of their homes. But one of the most important things to understand before applying is the interest rate you’ll pay. Home equity loan rates can change a lot depending on your lender, your credit score, and the economy. If you’re thinking about using your home’s equity, comparing rates can save you thousands of dollars. In this article, you’ll see how rates work, what affects them, and how to compare options like a pro.

What Is A Home Equity Loan Rate?

A home equity loan rate is the interest you pay on money borrowed against your home’s value. It is usually a fixed rate, meaning your payment stays the same for the life of the loan. This is different from a home equity line of credit (HELOC), which often has a variable rate. Knowing your rate helps you understand the true cost of borrowing.

Most home equity loan rates are lower than credit cards or personal loans because your home is the collateral. However, these rates are still higher than the original mortgage rates. The average fixed rate for a home equity loan in the US in early 2024 was around 7.5%–9%.

Key Factors That Affect Home Equity Loan Rates

Not all home equity loan rates are equal. Several factors play a big role:

- Credit Score: The higher your credit score, the lower your rate. For example, scores above 740 get the best rates, while scores below 650 may pay much more.

- Loan-to-Value Ratio (LTV): This is the percentage of your home’s value that you borrow. A lower LTV often means a better rate. Most lenders allow up to 80% LTV.

- Amount Borrowed: Large loans may have slightly higher rates.

- Repayment Term: Shorter terms (like 5 years) usually have lower rates than longer terms (like 15 years).

- Type of Loan: Fixed-rate home equity loans vs. variable-rate HELOCs.

- Lender Policies: Each lender sets its own rates and fees.

Here’s a quick look at how your credit score affects your rate:

| Credit Score | Typical Rate |

|---|---|

| 760+ | 7.25%–7.75% |

| 700–759 | 7.75%–8.50% |

| 660–699 | 8.50%–9.25% |

| 620–659 | 9.25%–10.50% |

Comparing Home Equity Loan Rates: What Matters Most

When you compare rates, don’t just look at the interest number. Look at the APR (annual percentage rate), which includes both the interest and any fees. This gives you a better idea of the real cost.

Other important things to compare:

- Closing costs: Can range from $0 to $2,000

- Origination fees: Usually 0%–2% of the loan amount

- Prepayment penalties: Some lenders charge if you pay off early

- Minimum and maximum loan amounts

- Repayment flexibility: Some loans allow interest-only payments for a period, but this is rare

Many borrowers miss these extra costs when comparing lenders. Always check the APR, not just the rate.

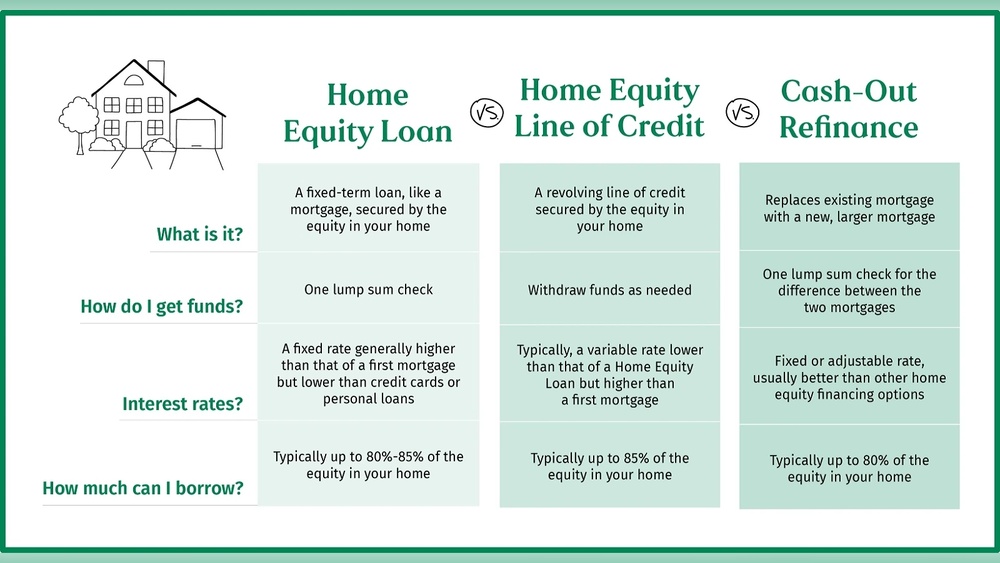

Home Equity Loan Vs. Heloc Rates

A home equity loan and a HELOC are not the same, even though both use your home’s value. The main difference:

- Home equity loan: Fixed rate, set payment, lump sum

- HELOC: Variable rate, flexible borrowing, can change over time

Here’s a quick comparison:

| Type | Interest Rate | Payment Type | Borrowing Style |

|---|---|---|---|

| Home Equity Loan | Fixed (7.5%–9%) | Same each month | Lump sum |

| HELOC | Variable (8%–10%) | Can change | Draw as needed |

Many people choose a home equity loan for big expenses with clear costs, like home renovations or debt consolidation. HELOCs work better for ongoing needs, but the rate can rise.

How To Find The Best Home Equity Loan Rates

Finding the best rate takes a bit of work. Here’s a step-by-step guide:

- Check your credit score: Fix mistakes and pay down debt if you can.

- Shop around: Get quotes from at least three lenders—banks, credit unions, online lenders.

- Compare APRs: Not just the interest rate.

- Look at fees: Origination, closing costs, and any extra charges.

- Ask about discounts: Some lenders offer better rates if you have other accounts with them.

- Read reviews: See how lenders treat their customers.

Don’t just rely on your current bank. Sometimes credit unions or online lenders offer better deals.

Real-world Rate Examples (2024)

To give you a clearer picture, here’s a comparison of rates from top US lenders in April 2024. Rates change often, so always check the latest.

| Lender | Fixed Rate | APR | Typical Fees |

|---|---|---|---|

| Wells Fargo | 7.99% | 8.25% | $0–$1,500 |

| Bank of America | 7.49% | 7.95% | $0–$1,200 |

| Chase | 8.25% | 8.75% | $500–$2,000 |

| US Bank | 7.75% | 8.10% | $0–$1,000 |

| Local Credit Union | 7.25% | 7.80% | $300–$1,000 |

Notice how credit unions often offer lower rates and fees. But national banks may have faster approval or easier online applications.

How Rate Changes Affect Your Loan Cost

Even small differences in rates can mean big savings or costs over time. Let’s look at an example:

If you borrow $50,000 with a 10-year term:

- At 7.5% rate: You pay about $596 per month, and $21,500 in interest over the life of the loan.

- At 8.5% rate: You pay about $619 per month, and $24,280 in interest total.

That’s nearly $2,800 more just for a 1% higher rate. This is why comparing carefully matters.

Tips For Getting Lower Home Equity Loan Rates

Want the best deal? Try these strategies:

- Improve your credit score: Even a small increase can unlock better rates.

- Lower your debt: Lenders check your debt-to-income ratio.

- Choose a shorter term: A 5-year loan usually has a lower rate than a 15-year loan.

- Borrow less: Lower LTV means lower risk for the lender.

- Shop around: Don’t accept the first offer.

- Consider credit unions: They often have better rates for members.

Some borrowers forget to ask about discounts. For example, linking a checking account or setting up automatic payments can reduce your rate.

Common Mistakes When Comparing Home Equity Loan Rates

Many people make mistakes when comparing rates. Here are a few you should avoid:

- Ignoring APR: Only looking at the interest rate can hide fees.

- Not checking fees: Closing costs and origination fees can add up.

- Choosing a variable rate: If you want steady payments, stick with a fixed rate.

- Not reading the fine print: Some loans have hidden penalties.

- Forgetting about credit unions: These often offer lower rates but are overlooked.

When Is A Home Equity Loan A Good Choice?

A home equity loan is best for:

- Home repairs or improvements

- Debt consolidation

- Large medical expenses

- Tuition payments

It’s less suitable for everyday spending or if your financial situation is unstable. Remember, your home is at risk if you don’t pay.

Latest Market Trends And Insights

Home equity loan rates have risen in recent years as the Federal Reserve raised interest rates. In 2022, average rates were about 6%–7%; now in 2024, they’re closer to 7.5%–9%. Some experts expect rates to stay high through the year.

Many homeowners are using equity loans because home prices have increased. This means more available equity, but higher rates mean higher monthly payments.

If you want more details on rate trends, check the Federal Reserve’s official site for updates.

Frequently Asked Questions

What Is The Average Home Equity Loan Rate In 2024?

The average fixed rate is between 7.5% and 9% in the US. Your own rate will depend on credit score, lender, and loan amount.

How Does My Credit Score Affect My Home Equity Loan Rate?

A higher credit score gets you a lower rate. For example, scores above 740 may qualify for rates under 7.5%, while scores below 660 can see rates above 9%.

Are Home Equity Loan Rates Fixed Or Variable?

Most home equity loans have fixed rates. HELOCs usually have variable rates that can change over time.

Can I Negotiate My Home Equity Loan Rate?

Yes, you can often negotiate rates, especially with credit unions or smaller banks. Ask about discounts or special offers.

What Fees Should I Expect With A Home Equity Loan?

Typical fees include closing costs ($0–$2,000), origination fees (up to 2%), and sometimes prepayment penalties. Always check the APR for the total cost.

Finding the right home equity loan rate can save you money and make borrowing safer. Take time to compare, understand the numbers, and ask questions. The right choice can help you reach your goals without risking your home.

Read More:

- Best Personal Loan Rates: Unlock Top Offers for 2026

- Bad Credit Personal Loans Guaranteed Approval: Easy Access Today

- Compare Mortgage Lenders Online: Find the Best Rates Fast

- Debt Consolidation Loan Online: Simplify Your Finances Fast

- First Time Home Buyer Loan Programs: Your Ultimate Guide 2026

- Small Business Loan Pre Approval: Fast Track Your Funding Success

- Mortgage Pre Approval Online: Fast-Track Your Home Buying Success

- Best Mortgage Refinance Rates: Unlock Lower Payments Today