Business Line Of Credit Rates: What Every Owner Should Know

Getting the right funding can change the future of your business. One flexible option many owners use is a business line of credit. You only pay interest on the money you borrow, and you can reuse the funds as you repay. But, the real cost depends on the interest rates and fees. Understanding how these rates work is crucial, so you don’t pay more than necessary or miss out on better deals. This guide explains how business line of credit rates are set, what affects them, and how you can get the best terms for your situation.

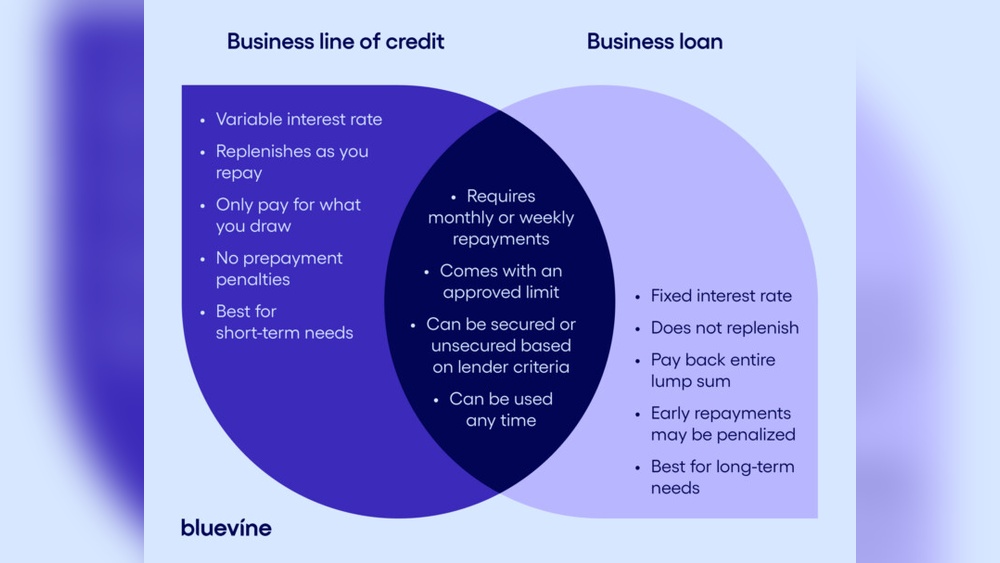

What Is A Business Line Of Credit?

A business line of credit is like a credit card for your business. You get access to a set amount of money, called the credit limit. You can borrow any amount up to this limit, repay it, and borrow again. It’s useful for covering cash flow gaps, buying inventory, or handling emergencies.

Unlike a loan, you don’t get all the money at once. You only pay interest on what you use. Rates vary depending on the lender, your credit score, and your business history. Most lines of credit are revolving, meaning you can keep using them as long as you pay back what you owe.

Typical Business Line Of Credit Rates

Business line of credit rates are not fixed. They depend on many factors, including your risk profile and market conditions. Here are some common ranges:

- Traditional Banks: 7% to 25% APR (Annual Percentage Rate)

- Online Lenders: 10% to 60% APR

- Credit Unions: 6% to 18% APR

Rates can change quickly, especially if the Federal Reserve raises interest rates. Here’s a comparison table showing typical rates for different lenders:

| Lender Type | APR Range | Typical Credit Limit |

|---|---|---|

| Bank | 7% – 25% | $25,000 – $500,000 |

| Online Lender | 10% – 60% | $1,000 – $250,000 |

| Credit Union | 6% – 18% | $10,000 – $100,000 |

Many beginners overlook that rates can be variable. This means the rate might change with the market. Some lenders also charge extra fees, which can increase your total cost.

Factors That Affect Business Line Of Credit Rates

Several things influence the rate you get for your business line of credit:

- Business Credit Score: Higher scores get lower rates. Aim for at least 680 for better offers.

- Revenue and Cash Flow: Lenders look for steady income.

- Time in Business: Older businesses (2+ years) usually get better rates.

- Collateral: Secured lines (backed by assets) have lower rates than unsecured ones.

- Industry: Risky industries, like restaurants or construction, often face higher rates.

Here’s another data table to show how credit score impacts rates:

| Credit Score Range | Estimated APR |

|---|---|

| 750 – 850 | 7% – 12% |

| 680 – 749 | 13% – 24% |

| 600 – 679 | 25% – 40% |

| Below 600 | 40%+ |

A common mistake is focusing only on the interest rate. Many owners forget to check draw fees, maintenance fees, or early repayment penalties. These can make a big difference in the real cost.

How To Get The Best Rates

Securing a low rate is not just about luck. You can actively improve your chances by following these steps:

- Improve Your Credit Score: Pay debts on time and keep balances low.

- Show Strong Financials: Prepare clear profit and loss statements.

- Shop Around: Compare offers from banks, online lenders, and credit unions.

- Offer Collateral: If possible, use business assets to secure the line.

- Negotiate: Don’t accept the first offer. Ask about lower rates or fee waivers.

Many beginners miss the value of relationship banking. If you have a history with a bank, they may offer better terms. Also, some lenders give discounts for automatic payments.

Fixed Vs. Variable Rates

Business lines of credit usually have variable rates, which means the cost can change over time. Some lenders offer fixed rates for short periods, but these are rare.

A fixed rate stays the same for a set period. This helps with budgeting, but you may pay more if the market rates fall. Variable rates are lower at first, but can rise. Decide what fits your risk tolerance.

Here’s a quick comparison:

| Type | Pros | Cons |

|---|---|---|

| Fixed Rate | Predictable payments | Can be higher than market rates |

| Variable Rate | Lower initial cost | Payments can increase |

Real-life Example

Imagine a small business owner, Maria, who needs $50,000 for inventory. She has a 720 credit score and 3 years in business. Her bank offers a 10% APR line of credit. Maria only uses $10,000 for two months. She pays interest only on what she borrows, saving money compared to a traditional loan.

Many owners forget that using less than the full limit keeps costs low. It’s a smart way to manage cash flow and avoid overpaying.

Hidden Costs And Common Mistakes

Besides interest, look out for:

- Draw Fees: Charged every time you withdraw funds

- Annual Fees: For keeping the line open

- Inactivity Fees: If you don’t use the line

- Late Payment Fees: If you miss a payment

Some owners make the mistake of using a line of credit for long-term needs. It’s best for short-term gaps, not big purchases like equipment.

Another overlooked tip: Check if the lender reports to credit bureaus. This can help your business build credit for future loans.

For more information on rates and trends, see the official Federal Reserve site.

Frequently Asked Questions

What’s The Average Rate For A Business Line Of Credit?

The average APR ranges from 7% to 25% at banks, but can be higher with online lenders. Your exact rate depends on your credit score, revenue, and business history.

Are Business Line Of Credit Rates Fixed Or Variable?

Most lines offer variable rates. These change with the market, so your payments can go up or down. Fixed rates are less common.

How Can I Lower My Business Line Of Credit Rate?

Improve your credit score, show strong financials, and compare offers. Offering collateral can help you get a better rate.

What Fees Besides Interest Should I Expect?

Watch for draw fees, maintenance fees, and annual fees. Always ask lenders for a full fee list before accepting an offer.

Can Startups Get A Business Line Of Credit?

It’s possible, but startups often pay higher rates and get smaller limits. Building business credit and revenue helps you qualify for better terms later.

Getting the best business line of credit rates takes knowledge and effort. By understanding how rates work and what affects them, you can make smarter choices and save money. Don’t forget to compare offers, ask questions, and check the fine print before signing any agreement.

Read More:

- Best Personal Loan Rates: Unlock Top Offers for 2026

- Bad Credit Personal Loans Guaranteed Approval: Easy Access Today

- Compare Mortgage Lenders Online: Find the Best Rates Fast

- Debt Consolidation Loan Online: Simplify Your Finances Fast

- First Time Home Buyer Loan Programs: Your Ultimate Guide 2026

- Home Equity Loan Rates Comparison: Find the Best Deals Today

- Small Business Loan Pre Approval: Fast Track Your Funding Success

- Mortgage Pre Approval Online: Fast-Track Your Home Buying Success